-

Housing inventory rose for the 19th month, with new listings up nationwide. See market trends, inventory stats, and expert advice for buyers and sellers. The U.S. housing market continues to shift, with inventory rising for the 19th straight month and new listings increasing across every major reg

Read More What’s Next for the 2025 Housing Market? Here’s What Experts Predict

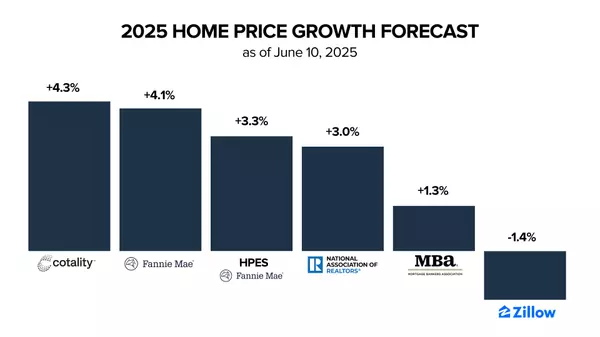

The 2025 housing market forecast highlights home prices, mortgage rates, and sales trends to help buyers and sellers navigate the second half of the year. Can you believe we’re already halfway through 2025? As we head into the second half of the year, a lot of buyers and sellers are asking the same

Read MoreThe Resurgence of Multigenerational Living: A Smart Solution for Modern Families

Discover why multigenerational living is making a comeback in today’s housing market. Learn about the benefits, design ideas, and how this lifestyle can help families manage rising home costs, caregiving, and more. As home prices and living expenses continue to rise, more families are turning to mu

Read MoreWhy 36% of Americans Choose Real Estate for Long-Term Wealth

Discover why real estate remains the top long-term investment for Americans. More people prefer real estate over stocks, bonds, and cryptocurrencies. When it comes to long-term investments, Americans have a clear favorite: real estate. According to a recent Gallup poll, 36% of Americans believe r

Read MoreZillow Home Value and Home Sales Forecast (April 2025) What You Need to Know

Get the latest insights on the housing market with Zillow's home value and home sales forecast for April 2025. Learn about current trends, forecasts, and what it means for homebuyers and sellers. As we enter the spring season, the housing market is expected to continue its upward trend. In thi

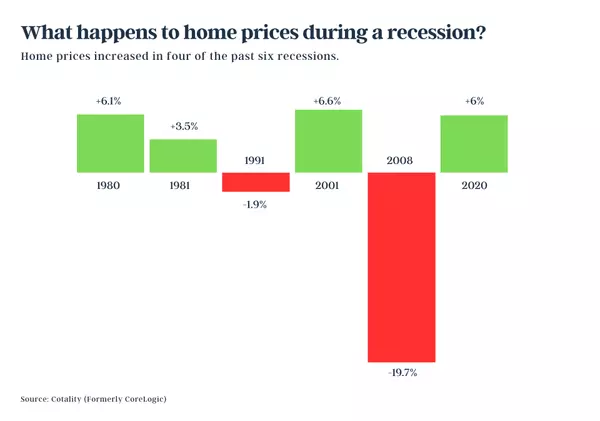

Read MoreWhat Really Happens to Home Prices During a Recession?

Curious what happens to home prices during a recession? Historical data reveals surprising trends that could impact your real estate decisions in today's market. Every time the word "recession" starts popping up in headlines, it brings a wave of uncertainty—especially for anyone thinking about buyi

Read MoreVirginia Beach Real Estate Market Trends

Stay up-to-date on the latest Virginia Beach real estate market trends. Learn about current housing market conditions, mortgage rates, and home prices. Get expert insights on the local real estate market. The Virginia Beach housing market is experiencing a mix of trends that are shaping

Read MoreSpring into Action: Navigating the Current Real Estate Market Trends

The real estate market is constantly evolving, and staying informed is key to making the most of the current conditions. As we head into the new season, it's essential to understand the latest market trends and how they may impact your buying or selling experience. For sellers, the news is lar

Read MoreRing in the New Year with a Fresh Start: Bucket List & Home Refresh Tips

As we embark on a fresh year, many of us are eager to set new goals and embrace new beginnings. This year, why not incorporate some home-related resolutions into your plans? A clean and organized living space can significantly impact your overall well-being. Around-the-House Refresh Tasks: Deep Cl

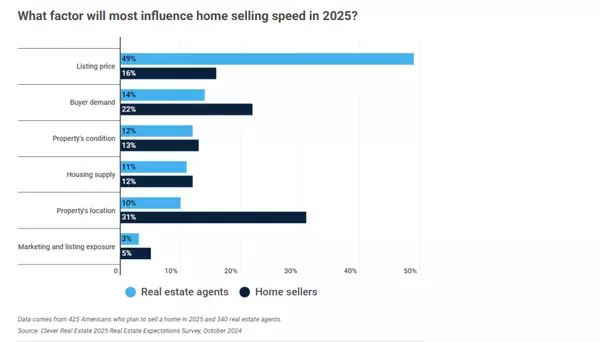

Read MoreBridging the Gap: Buyer and Seller Expectations in the 2025 Housing Market

A recent survey by Clever Real Estate revealed a significant disconnect between buyer and seller expectations in the 2025 housing market, particularly when it comes to pricing and timelines. This presents both challenges and opportunities for real estate professionals like you. The Price Gap: A Maj

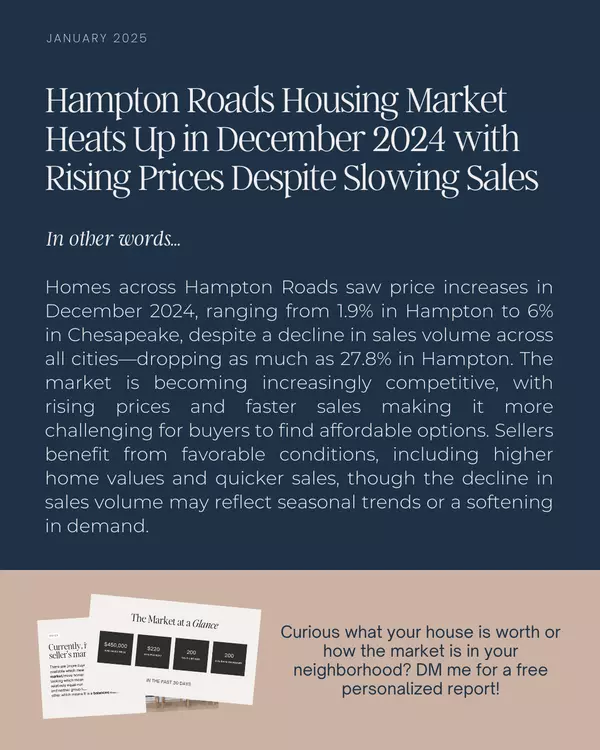

Read MoreNavigating the Shifting Tides: Hampton Roads Real Estate Market Review

Market Update: A November to Remember In November 2024, the Hampton Roads real estate market showcased a notable increase, reflecting a broader trend of growth and resilience in the region. This month has been particularly significant for both buyers and sellers, as the market dynamics have shifted

Read MoreNavigating the Waves: October 2024 Hampton Roads Real Estate Market Report

The Hampton Roads real estate market has shown resilience and growth throughout October 2024. With rising home prices, an uptick in settled sales, and a steady increase in available inventory, the region remains a hotspot for buyers and investors alike. Market OverviewIn October, the Hampton Roads

Read MoreTwo Reasons Why the Housing Market Won’t Crash

You may have heard chatter recently about the economy and talk about a possible recession. It’s no surprise that kind of noise gets some people worried about a housing market crash. Maybe you’re one of them. But here’s the good news – there’s no need to panic. The housing market is not set up for

Read MoreThe residential market across Hampton Roads shows significant trends for September 2024

Hampton Roads's residential real estate market is showcasing noteworthy trends as we move through September 2024. Here’s a closer look at the current landscape: Market Overview Median Sales Price: The average home price in the region is now $356,500, reflecting a modest 0.4% increase. This st

Read More

Categories

Recent Posts

DISCOVER VIRGINIA BEACH WITH ME!

LIVE LIKE A LOCAL

A curated selection of my favorite stores, restaurants, fun things to do, or places to grab a drink around town.